Tahoe Mountain Realty August 2016 Market Report

Real Estate Market Figures Speak for Themselves with Over $160M in Total Sales Volume

Truckee, CA: In reviewing the performance of Tahoe-Truckee real estate for the month of August, the figures speak for themselves.

August 2016:

- 178 residential transactions: The greatest number in any month since 2005 and 30 transactions more than any other month in 2016.

- $160,154,290 in total sales volume: Added a full 20% to the previous 8 months. This month alone would have accounted for 25% of total volume in 2009.

- $899,743 average sale price: While not the greatest single monthly average this year, when factoring in the volume of sales, many of which are likely to be in the lower price tiers, a remarkable figure and the single highest for the month of August since 2005.

Year-to-Date:

- 1001 total transactions through 8 months exceeds the 12-month total of many prior years.

- $851,163,973 total sales volume: Already exceeds 12-month totals for each year from 2007-2012

- $850,314 average sale price: 13% higher than 2015 and the first time this metric exceeds 2006-2007. Median price has risen 4% over the same period.

- Sales greater than $1,000,000 and $2,000,000 have already exceeded the total number in 2015.

While nearly all sectors of the market showed gains in August, the most notable driver was Martis Camp with 10 homes sales that accounted for 23% of total volume for the month. At an average price of $3,711,950 and $1,163 per square foot, Martis Camp continues to transcend the luxury space for the region. Additionally, 3 lakefront properties traded between $2,690,000 - $6,500,000. Lahontan closed 4 homes from $1,590,000 - $2,250,000, Gray’s Crossing saw 3 trades from $1,370,000 to $1,735,000; the latter representing the highest pricing in that community this year.

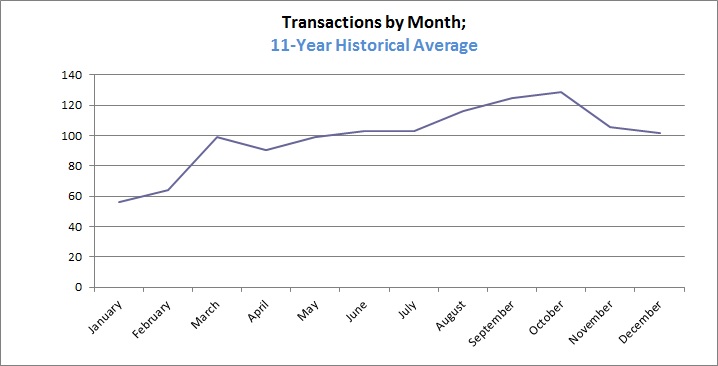

Perhaps most remarkably, this exceptional 30-day period comes just ahead of the typical surge for Tahoe-Truckee homes sale. Under normal market conditions, consumers will shop for real estate through Labor Day before making a purchasing decision in anticipation of the winter season to come. As such, September and October are most often the peak months for real estate closings in our region. With over 200 transactions currently pending, September appears to be on a similar trajectory.

Despite this strong absorption, there remains ample inventory of over 9 months supplying the market. It is not unreasonable to expect some cooling as we move beyond the current landscape. The same normalized market conditions that show surging sales over the next 60 days indicate a steep drop off from November – January. Similarly, election years generally create some level of paralysis for discretionary purchases including resort real estate. Particularly in a year as volatile as this, some level of market uncertainly can be expected. Finally, surging conditions like we are now experiencing are often followed almost immediately by a cooling. Without the major debt overhang of a decade ago, this cooling is likely to be a leveling of prices and slightly extended market time rather than more significant impacts in the not-too-distant past.